Enterprise AI crossed a threshold in 2026: adoption is nearly universal, spending is measured in trillions, and the gap between the companies capturing real value and everyone else is widening fast. This page collects the most-cited enterprise AI statistics of 2025–2026 in one place, adoption, spend, token economics, ROI, developer impact and workforce shifts, every number traced to a named analyst firm, primary survey or vendor research report and quoted faithfully.

Key Enterprise AI Statistics

If you only cite eight numbers about enterprise AI in 2026, cite these.

- 88% of organizations now regularly use AI in at least one business function. (Source: McKinsey State of AI survey, 2025)

- Worldwide AI spending will total $2.59 trillion in 2026, a 47% increase over 2025. (Source: Gartner, 2026)

- Enterprises spent $37 billion on generative AI in 2025, up from $11.5 billion in 2024, a 3.2x increase in a single year. (Source: Menlo Ventures, State of Generative AI in the Enterprise, 2025)

- 95% of enterprise generative AI pilots fail to deliver measurable P&L impact. (Source: MIT Project NANDA, The GenAI Divide, 2025)

- 79% of enterprises experienced AI cost overruns in the past 12 months. (Source: DoiT survey of 500 finance leaders, conducted by Sapio Research, 2026)

- 84% of software developers use or plan to use AI tools, but 46% actively distrust the accuracy of AI output. (Source: Stack Overflow Developer Survey, 2025)

- Workers with AI skills command a 62% average wage premium, up from 56% a year earlier. (Source: PwC Global AI Jobs Barometer, 2026)

- LLM inference prices are falling at a median rate of 50x per year across performance milestones, accelerating to a median of 200x per year since January 2024. (Source: Epoch AI, 2025)

Market Size and Investment

Global AI spending will reach $2.59 trillion in 2026, roughly 41% of all IT spending, and nearly $1 trillion more than in 2025. (Gartner, 2026 )

- Global corporate AI investment reached $581.7 billion in 2025, up 130% from the prior year. (Source: Stanford HAI AI Index Report, 2026)

- Private AI investment hit $344.7 billion in 2025, an increase of 127.5% from 2024. US investments ($285.9 billion) were 23.1 times greater than those of the next-highest country. (Source: Stanford HAI AI Index Report, 2026)

- More than 45% of all AI spending goes toward infrastructure, AI-optimized servers, chips, network fabric and compute. Spending on AI-optimized servers is expected to triple over the next five years. (Source: Gartner, 2026)

- Data center spending will grow 55.8% in 2026 to surpass $788 billion. (Source: Gartner, 2026)

- Spending on AI models is set to nearly double from more than $32 billion in 2025 to nearly $60 billion by 2027. (Source: Gartner, 2026)

- Enterprise generative AI revenue grew from $1.7 billion in 2023 to $37 billion in 2025, the fastest-scaling software category in history, now 6% of the global SaaS market. (Source: Menlo Ventures, 2025)

- Of 2025’s $37 billion in enterprise genAI spend, applications captured $19 billion and infrastructure $18 billion. Foundation model APIs alone accounted for $12.5 billion. (Source: Menlo Ventures, 2025)

- Organizations increased AI compute spending 166% year-over-year in Q2 2025, with AI compute and storage hardware reaching roughly $82 billion in that quarter alone. (Source: IDC, 2025)

US enterprise generative AI spend (Menlo Ventures, 2025): $1.7B in 2023 → $11.5B in 2024 → $37B in 2025.

| Gartner AI spending forecast | Figure | Change |

| Total worldwide AI spending, 2026 | $2.59 trillion | +47% vs 2025 |

| AI agent software, 2026 | $206.5 billion | → $376.3B in 2027 (+82%) |

| Data center spending, 2026 | $788+ billion | +55.8% vs 2025 |

| AI model spending, 2025 → 2027 | $32B → ~$60B | ~2x in two years |

Enterprise Adoption and Usage

88% of organizations regularly use AI in at least one business function but nearly two-thirds have not yet begun scaling AI across the enterprise. (McKinsey State of AI survey, 2025 )

- 72% of organizations report using generative AI, up from 33% in 2024. (Source: McKinsey State of AI survey, 2025)

- 62% of organizations are at least experimenting with AI agents, and 23% are scaling an agentic AI system somewhere in the enterprise. (Source: McKinsey State of AI survey, 2025)

- Only 17% of organizations have deployed AI agents to date but more than 60% say they expect to within the next two years. (Source: Gartner, 2026)

- 76% of enterprise AI use cases are now purchased rather than built internally, a sharp reversal from the year before, when 53% were built in-house. (Source: Menlo Ventures, 2025)

- 47% of AI deals go to production, compared with 25% for traditional SaaS. (Source: Menlo Ventures, 2025)

- 27% of all AI application spend arrives through product-led growth motions, nearly 4x the 7% rate in traditional software. (Source: Menlo Ventures, 2025)

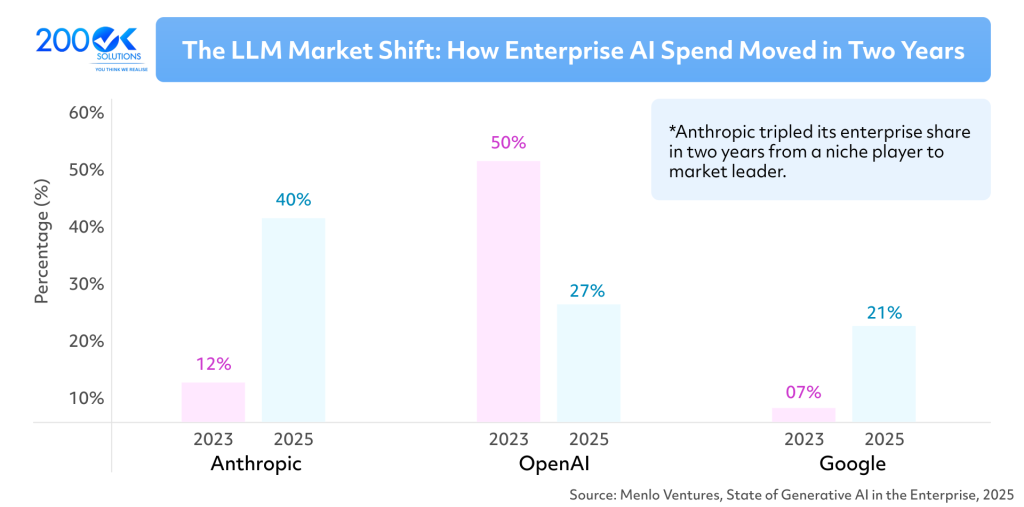

- Anthropic holds 40% of enterprise LLM API spend (up from 12% in 2023), OpenAI 27% (down from 50% in 2023), and Google 21% (up from 7% in 2023). (Source: Menlo Ventures, 2025)

- Open-source models’ share of enterprise LLM usage fell to 11%, down from 19% in 2024. (Source: Menlo Ventures, 2025)

AI Costs and Token Economics

The paradox of 2026: per-token prices are collapsing while total AI bills explode. Usage-based pricing, agent workloads and hidden platform costs make AI the hardest line item in the IT budget to forecast.

80–85% of enterprises miss their AI infrastructure forecasts by more than 25%. ( Mavvrik & BenchmarkIT, State of AI Cost Management Research, 2025 )

- 79% of enterprises experienced AI cost overruns in the past 12 months. (Source: DoiT survey of 500 US/UK finance leaders, conducted by Sapio Research, February 2026)

- Counterintuitively, 89% of organizations that rate themselves very mature on FinOps experienced AI cost overruns with a mean overspend of 30.9%, the highest of any segment. (Source: DoiT / Sapio Research, 2026)

- Only 15% of finance leaders can calculate AI ROI without significant bottlenecks. (Source: DoiT / Sapio Research, 2026)

- 83% of finance leaders expect clear, quantifiable AI returns within 12 months, and 81% are already adjusting AI spend or plan to within the year. (Source: DoiT / Sapio Research, 2026)

- The share of companies allocating at least a quarter of their IT budget to AI is expected to nearly double, from 27% to 52%. (Source: EY AI-Driven Productivity and Investment Survey, 2025)

- Companies plan to spend 1.7% of revenue on AI in 2026, up from 0.8% in 2025. (Source: BCG, As AI Investments Surge, CEOs Take the Lead, 2026)

- Only 6% of executives would reduce AI investments if current initiatives fail to deliver in 2026, 94% will keep investing despite uncertain returns. (Source: BCG AI Radar, 2026)

- LLM inference prices have fallen between 9x and 900x per year depending on the performance milestone, with a median of 50x annually and a median of 200x per year since January 2024. (Source: Epoch AI, 2025)

- The price to achieve GPT-4-level performance on PhD-level science questions fell by 40x per year. (Source: Epoch AI, 2025)

Table: AI cost overruns by FinOps maturity. Source: DoiT survey conducted by Sapio Research, February 2026 (n=500 finance leaders, US & UK, 1,000+ employee organizations).

| Segment | Experienced AI cost overruns | Mean overspend |

| All enterprises surveyed | 79% | — |

| Very mature / leading-edge FinOps | 89% | 30.9% |

| Early-stage FinOps | 69% | 16.1% |

ROI and Business Impact

95% of enterprise generative AI pilots fail to deliver measurable P&L impact, only 5% of projects create measurable financial value. MIT Project NANDA, The GenAI Divide, 2025 (300+ deployments, 52 case studies, 153 leadership surveys)

- Only 39% of organizations report any EBIT impact attributable to AI at the enterprise level. (Source: McKinsey State of AI survey, 2025)

- Roughly 6% of organizations qualify as AI high performers, attributing more than 5% of EBIT to AI. (Source: McKinsey State of AI survey, 2025)

- AI high performers are 2.8x more likely to have fundamentally redesigned workflows around AI (55% vs 20% of other organizations). (Source: McKinsey State of AI survey, 2025)

- 65% of AI high performers have defined human-in-the-loop validation processes, versus 23% of other organizations. (Source: McKinsey State of AI survey, 2025)

- Buying AI tools from specialized vendors and building partnerships succeeds about 67% of the time, internal builds succeed only a third as often. (Source: MIT Project NANDA, 2025)

- More than half of generative AI budgets go to sales and marketing tools, yet the biggest measured ROI is in back-office automation, cutting BPO and external agency costs. (Source: MIT Project NANDA, 2025)

- Organizations using AI coding tools report 15%+ velocity gains in software delivery. (Source: Menlo Ventures, 2025)

AI in Software Development

84% of developers use or plan to use AI tools in their development process yet more developers actively distrust AI output accuracy (46%) than trust it (33%). Stack Overflow Developer Survey, 2025 (49,000+ respondents, 177 countries)

- 51% of professional developers use AI tools daily. (Source: Stack Overflow Developer Survey, 2025)

- 66% of developers say their biggest frustration is “AI solutions that are almost right, but not quite” and 45% say debugging AI-generated code is more time-consuming. (Source: Stack Overflow Developer Survey, 2025)

- Positive sentiment toward AI tools fell from over 70% in 2023–2024 to 60% in 2025, and only 3% of developers “highly trust” AI output. (Source: Stack Overflow Developer Survey, 2025)

- 31% of developers use AI agents, but 52% either avoid agents entirely or stick to simpler tools; 75.3% still ask another person when they don’t trust an AI answer. (Source: Stack Overflow Developer Survey, 2025)

- Enterprise spend on AI coding tools grew from $550 million in 2024 to $4 billion in 2025, the largest departmental AI category, at 55% of departmental spend. (Source: Menlo Ventures, 2025)

- Anthropic holds 54% enterprise market share in coding workloads, up from 42% six months prior; OpenAI holds 21%. (Source: Menlo Ventures, 2025)

- 50% of developers now use AI coding tools daily, rising to 65% in top-quartile organizations. (Source: Menlo Ventures, 2025)

- Employment of young software developers (ages 22–25) has fallen nearly 20% since 2024. (Source: Stanford HAI AI Index Report, 2026)

- Cursor reached $200 million in revenue before hiring a single enterprise sales rep, a sign of how product-led growth dominates AI dev tooling. (Source: Menlo Ventures, 2025)

Workforce and Skills

Workers with AI skills earn a 62% average wage premium in 2026, up from 56% in 2025 and 25% the year before, reaching 118% in consumer markets.(PwC Global AI Jobs Barometer, 2026 )

- Since generative AI’s proliferation in 2022, productivity growth has nearly quadrupled in the industries most exposed to AI from 7% (2018–2022) to 27% (2018–2024). (Source: PwC Global AI Jobs Barometer, 2025)

- The skills employers seek are changing 66% faster in occupations most exposed to AI, up from 25% the year before. (Source: PwC Global AI Jobs Barometer, 2025)

- Jobs “professionalised” by AI are growing twice as fast as jobs “democratised” by AI, with 42% faster wage growth since 2021. (Source: PwC Global AI Jobs Barometer, 2026)

- The share of AI-augmented jobs requiring a formal degree fell from 66% to 59% between 2019 and 2024. (Source: PwC Global AI Jobs Barometer, 2025)

- New tasks added to AI-exposed roles are 2.5x more likely to rely on human skills like empathy, judgement and creativity. (Source: PwC Global AI Jobs Barometer, 2026)

- Four out of five US high school and college students now use AI. (Source: Stanford HAI AI Index Report, 2026)

Challenges and Risks

The failure modes are as well-documented as the successes and they’re mostly organizational, not technical. As MIT’s researchers put it, the divide “does not seem to be driven by model quality or regulation, but seems to be determined by approach.”

- 51% of organizations have experienced at least one negative consequence from AI use; inaccuracy is the most common issue, reported by 30%. (Source: McKinsey State of AI survey, 2025)

- Over 40% of agentic AI projects will be canceled by the end of 2027. (Source: Gartner, 2026)

- Only 16% of enterprise AI deployments (and 27% at startups) qualify as true agents, systems with planning, execution and adaptive behavior. (Source: Menlo Ventures, 2025)

- About 85% of organizations misestimate AI costs by more than 10%, and nearly a quarter are off by 50% or more. (Source: Mavvrik & BenchmarkIT, 2025)

- There is a 33-point gap between how mature C-suite leaders believe their AI cost management is (93% say mature) and how managers on the ground rate it (60%). (Source: DoiT / Sapio Research, 2026)

- AI data center power capacity has reached 29.6 GW, roughly what it takes to power the entire state of New York at peak demand. (Source: Stanford HAI AI Index Report, 2026)

Future Projections

AI agent software spending will hit $206.5 billion in 2026 and jump 82% to $376.3 billion in 2027. (Gartner, 2026 )

- 40% of enterprise applications will feature task-specific AI agents by the end of 2026, up from less than 5% at the start of the year. (Source: Gartner, 2026)

- Enterprises will more than double their spending on generative AI models and AI agents in 2026, “enterprises have yet to really flex their spending potential. That is coming and 2026 will be the inflection year,” per Gartner analyst John-David Lovelock. (Source: Gartner, 2026)

- The estimated value of generative AI tools to US consumers reached $172 billion annually by early 2026, with median value per user tripling between 2025 and 2026. (Source: Stanford HAI AI Index Report, 2026)

- The share of companies allocating at least half their IT budget to AI is expected to rise from 3% to 19%. (Source: EY AI-Driven Productivity and Investment Survey, 2025)

- At least 10 AI products now generate more than $1 billion in annual recurring revenue, and 50+ have crossed $100 million. (Source: Menlo Ventures, 2025)

Frequently Asked Questions

What percentage of companies use AI in 2026?

88% of organizations regularly use AI in at least one business function, and 72% use generative AI, up from 33% in 2024, according to McKinsey’s State of AI survey. However, nearly two-thirds have not yet begun scaling AI across the enterprise.

How much will be spent on AI in 2026?

Gartner forecasts worldwide AI spending will total $2.59 trillion in 2026, a 47% increase over 2025. More than 45% of that goes to AI infrastructure such as servers, chips and compute.

Why do AI budgets overrun so often?

79% of enterprises experienced AI cost overruns in the past 12 months (DoiT / Sapio Research, 2026), and 80–85% of enterprises miss their AI infrastructure forecasts by more than 25% (Mavvrik & BenchmarkIT, 2025). Usage-based token pricing, agent workloads and data platform costs make AI spend much harder to forecast than seat-based SaaS, even organizations with mature FinOps practices overran by a mean of 30.9%.

Do enterprise AI projects actually deliver ROI?

Most don’t yet: MIT’s Project NANDA found 95% of enterprise generative AI pilots fail to deliver measurable P&L impact, and McKinsey finds only 39% of organizations report any EBIT impact from AI. The roughly 6% of companies that qualify as AI high performers are 2.8x more likely to have fundamentally redesigned workflows around AI rather than layering it onto existing processes.

How is AI changing software development?

84% of developers use or plan to use AI tools (Stack Overflow, 2025) and 51% of professional developers use them daily. Enterprise spend on AI coding tools grew from $550 million to $4 billion in one year (Menlo Ventures). But trust is falling: 46% of developers actively distrust AI output accuracy, and 66% say their biggest frustration is AI solutions that are almost right but not quite.

Sources

Every statistic above is quoted from one of the following organizations’ research, surveys or forecasts (2025–2026 editions):

- McKinsey & Company (State of AI survey)

- Gartner

- Stanford HAI (AI Index Report 2026)

- Menlo Ventures (State of Generative AI in the Enterprise)

- MIT Project NANDA (The GenAI Divide)

- PwC (Global AI Jobs Barometer)

- Stack Overflow (Developer Survey 2025)

- Epoch AI

- DoiT / Sapio Research

- Mavvrik & BenchmarkIT

- EY

- BCG (AI Radar)

- IDC

You may also like : Context Engineering vs Prompt Engineering: What’s the Real Difference