Embedded finance is no longer a trend, it’s a structural shift. For decision-makers navigating financial technology today, the core question is no longer whether to embed financial services into your product, but who bears the risk, who captures the revenue, and how partnership economics must evolve to reflect that reality. If you’re a CTO, CEO, or COO evaluating your next fintech partnership, this is the strategic rethink you can’t afford to skip.

What Is Fintech, And Why the Definition Has Expanded

Fintech meaning has changed dramatically. The traditional fintech definition described technology companies that digitized banking, lending, or payments. Today, fintech significado is broader: it encompasses any business that embeds financial capabilities, credit, insurance, payments, investments, directly into non-financial products.

Think of a logistics SaaS platform offering invoice financing. Or an HR tool providing earned wage access. These are fintechs, even if they don’t call themselves one.

What is fintech in 2026? It is the infrastructure layer underneath commerce, distribution, and enterprise software.

The Embedded Finance Shift: What Decision-Makers Need to Understand Now

Traditional financial technology partnerships were straightforward: a bank or payment processor provided rails, and a fintech rode them in exchange for volume-based fees. That model is breaking.

Here’s what’s replacing it:

- Revenue share models where the non-bank distributor captures a meaningful percentage of net interest margin or interchange

- Risk transfer agreements that move credit risk, fraud exposure, or compliance liability to the party best positioned to manage it

- White-label financial products that let B2B SaaS companies monetize their customer relationships through embedded lending or insurance

- Contextual financial services triggered by behavioral data, not branch visits or loan applications

The economics of fin tech distribution have fundamentally changed because the customer relationship has moved. Fintechs and software platforms now own the primary touchpoint. Banks and insurers are becoming the infrastructure. And that shift in customer ownership demands a shift in how value is shared.

How Revenue Share Models Are Being Restructured

Legacy partnerships paid distributors a flat referral fee. New embedded finance arrangements operate more like joint ventures.

What modern revenue share looks like:

- Gross margin split on financial products : distributor receives 30–60% of net revenue generated from embedded loans, cards, or insurance sold to their user base

- Volume-based step-ups : as transaction volume scales, the distributor’s share increases, incentivizing growth

- Data monetization rights : partners with richer behavioral data negotiate premium economics because their underwriting signal is more valuable

- Loss-sharing floors : risk is co-held up to a defined default threshold, aligning incentives on credit quality

For CEOs and COOs evaluating financial technology partnerships today, the question is: are you negotiating like a referral partner, or like an economic co-owner?

Risk Transfer: The Hidden Variable in FinTech Partnership Negotiations

Revenue gets the headlines. Risk transfer determines whether those economics are sustainable.

Key risk categories now being actively negotiated:

- Credit risk: Who holds the loan on balance sheet? Who absorbs first-loss?

- Regulatory and compliance risk: Which entity is the licensed lender, money transmitter, or insurance agent and does that match operational reality?

- Fraud and chargeback exposure: How is liability allocated when embedded payment flows are compromised?

- Data risk: Who is accountable if the behavioral data used for underwriting proves biased or non-compliant?

Companies that approach embedded finance without structuring risk transfer explicitly often discover, after a credit cycle turns, that they absorbed exposure they never priced for. This is where intelligent business transformation becomes operational: aligning legal structure, technology architecture, and partnership contracts before a product launches, not after losses appear.

The New FinTech Distribution Model: A Strategic Framework for Decision-Makers

If you’re a CTO evaluating a fintech login or API integration, or a CEO assessing a new financial product line, use this framework:

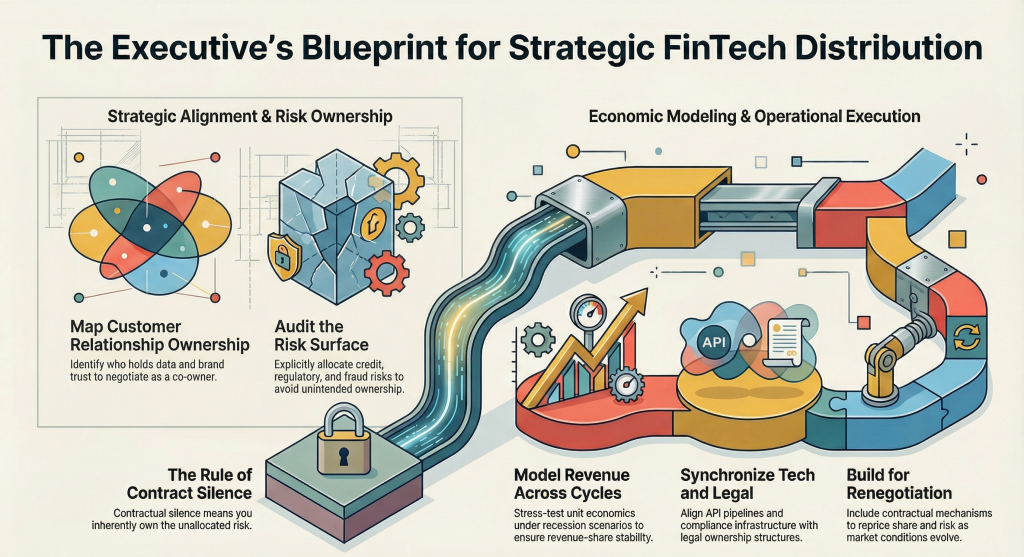

Step 1: Map the customer relationship ownership Who holds primary data, interaction frequency, and brand trust? That entity should negotiate as an economic co-owner, not a lead generator.

Step 2: Audit your risk surface before signing Identify every risk category, credit, regulatory, fraud, data and confirm explicit contractual allocation. Silence in a contract means you own the risk.

Step 3: Model revenue share across economic cycles Run unit economics under base, stress, and recession scenarios. A 50% revenue share on embedded lending collapses if default rates rise and you share the loss.

Step 4: Align technology architecture to partnership structure Your fintech API integrations, data pipelines, and compliance infrastructure must reflect who legally owns what. Misalignment creates both operational failure and regulatory exposure.

Step 5: Build for renegotiation Embedded finance partnerships have short equilibrium windows. Build contractual mechanisms to reprice revenue share and risk transfer as volume, data quality, and market conditions evolve.

FAQ: Embedded Finance and FinTech Partnership Economics

Q What is the fintech definition in the context of embedded finance?

A. Fintech or financial technology, now includes any platform that distributes financial products (credit, payments, insurance) natively within a non-financial software experience.

Q. How does revenue share work in embedded fintech models?

A. Partners share a percentage of net revenue generated from embedded financial products sold to their user base, structured around volume, risk co-ownership, and data contribution.

Q. What is risk transfer in a fintech partnership?

Risk transfer is the contractual allocation of credit, compliance, fraud, and data liability between the technology distributor and the licensed financial institution.

How should a CTO evaluate a fintech integration?

Evaluate API depth, data architecture alignment, compliance obligations, and whether the integration structure reflects your organization’s actual risk ownership.

200OK Solutions helps enterprise and fintech leaders design partnership models that are economically sound, technically integrated, and built for scale. Explore how intelligent business transformation applies to your financial product strategy at 200oksolutions.com.

You may also like: Customer Acquisition Costs Are Unsustainable: The Case for Lifetime Value-Led Growth in FinTech