FinTech companies that continue prioritizing customer acquisition over customer lifetime value (LTV) are building on a crumbling foundation. With CAC rising 60%+ over the last five years and funding winters forcing profitability conversations, the only sustainable growth model is one that maximizes revenue from customers you already have, powered by intelligent business transformation

Why CAC-Led Growth Is Breaking FinTech Business Models

Ask any FinTech CFO what keeps them up at night, and rising customer acquisition costs will be near the top of the list. Paid channels are saturated, app store competition is fierce, and consumers are more selective than ever about the financial products they trust.

The Numbers Don’t Lie

To understand the scale of this problem, consider what the data reveals:

- Average CAC for FinTech companies ranges from $200 to $1,500 depending on the product segment

- Churn rates in digital banking and lending often exceed 25% annually

- Payback periods on CAC now stretch 18–36 months for many consumer FinTech products

- Yet most growth budgets still allocate 70–80% toward acquisition over retention

As a result, this is not a marketing problem. It is a structural business model problem and it therefore requires a transformation-level response.

How to Shift from CAC-Led to LTV-Led Growth in FinTech

Shifting to lifetime value-led growth is not about spending less on acquisition. Instead, it’s about redesigning your entire customer operating model so that every dollar of acquisition spend generates compounding returns. Here is a proven five-step framework to get there.

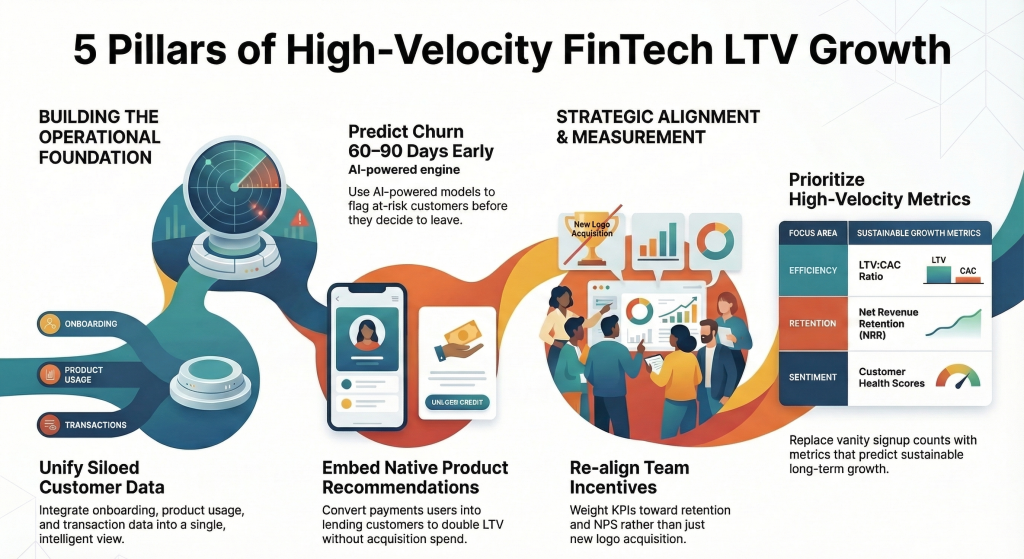

Step 1: Unify Your Customer Data

First and foremost, most FinTechs operate with siloed data across onboarding, product usage, support, and transactions. You cannot calculate true LTV, let alone act on it, without a single, intelligent view of the customer. Consequently, intelligent data integration must be your starting point before anything else.

Step 2: Predict Churn Before It Happens

Once your data is unified, AI-powered churn prediction models can flag at-risk customers 60–90 days before they leave. This creates intervention windows that retention teams can act on, through personalized offers, proactive support, and product nudges, instead of reacting after the fact.

Step 3: Build Cross-Sell and Upsell Into the Product Journey

Beyond churn prevention, the most LTV-efficient FinTechs don’t rely on outbound campaigns to expand revenue. Rather, they embed intelligent product recommendations directly into the customer experience. For example, a payments customer who becomes a lending customer doubles their LTV before you spend a single dollar on new acquisition.

Step 4: Align Incentives Across Teams

Even with the right technology in place, if your sales and growth teams are compensated purely on new logos, your organization remains structurally wired against LTV. Therefore, intelligent business transformation must include re-aligning KPIs so that retention, expansion, and NPS carry the same weight as net-new acquisition.

Step 5: Measure What Actually Matters

Finally, replace vanity metrics, installs, signups, month-over-month growth, with LTV:CAC ratio, net revenue retention (NRR), and customer health scores. These are the metrics that predict sustainable growth and that boards and investors increasingly demand.

The Business Outcomes FinTech Leaders Actually Care About

For CEOs, CTOs, and COOs evaluating this shift, the outcomes are tangible and measurable. Specifically, a well-executed LTV-led strategy delivers:

- Reduced burn rate : retaining a customer costs 5–7x less than acquiring a new one

- Improved unit economics : LTV:CAC ratios above 3:1 signal a fundable, scalable business

- Faster path to profitability : expansion revenue from existing customers carries no new CAC

- Competitive differentiation : while competitors race to acquire, you win by deepening relationships

- Investor confidence : NRR above 110% is one of the most powerful signals of business health

Importantly, these are not aspirational outcomes. They are the direct, proven result of intelligently transforming how your business serves and retains customers.

Why Intelligent Business Transformation Is the Missing Enabler

The reason most FinTechs struggle to execute an LTV-led strategy isn’t a lack of desire, it’s a lack of infrastructure and intelligence. Legacy systems don’t talk to each other, data teams are overwhelmed, and product and growth operate in silos.

Bridging the Gap Between Strategy and Execution

This is precisely where intelligent business transformation makes the difference. It brings together AI, process re-engineering, and technology modernization to give FinTech leaders the operational clarity they need to act on LTV opportunities in real time. Furthermore, it ensures that the shift is sustainable, not just a one-time initiative that fades when priorities change.

This isn’t about deploying a single tool. It’s about fundamentally rewiring how your business thinks, operates, and grows.

Frequently Asked Questions

Q: How do I calculate LTV accurately if my customer data is fragmented?

Start with a unified data layer that consolidates transactional, behavioral, and support data. Even so, a basic LTV model built on clean, connected data will outperform sophisticated models built on siloed inputs.

Q: How long does it take to shift from a CAC-led to an LTV-led growth model?

Most organizations begin seeing measurable NRR improvement within 6–9 months of implementing data unification and churn prediction. However, full model transition, including incentive realignment and product-led expansion , typically takes 12–18 months.

Q: What’s the right LTV:CAC ratio for a FinTech company?

A ratio of 3:1 is the commonly accepted benchmark for a healthy business. Ratios above 4:1 indicate significant headroom to invest more aggressively in growth. Below 2:1, on the other hand, signals that unit economics need attention before scaling.

Q: Can smaller FinTechs implement LTV-led growth without massive technology investment?

Yes. The starting point is data visibility, not infrastructure overhaul. In fact, many organizations achieve significant wins by simply connecting product analytics, CRM, and support data before investing in new platforms.

The Bottom Line for FinTech Decision-Makers

Ultimately, the FinTechs that will win the next five years are not those who acquire the most customers. They are those who build the deepest, most valuable relationships with the customers they already have.

LTV-led growth is not a strategy for slow companies. On the contrary, it is the strategy for smart ones.

If you’re a FinTech CEO, CTO, or COO asking how to reduce CAC dependency and build a more resilient growth engine, 200OK Solutions can help you get there. Our intelligent business transformation practice is built specifically for organizations ready to grow differently.

You may also like: The Compliance Cost Curve Is Steepening and Most FinTechs Are Not Structured to Absorb It