FinTech boards facing regulatory scrutiny in 2025 need to close a dangerous governance gap now. Across global financial hubs from Singapore to Scotland, regulators are moving faster than most boards realise. The question is no longer whether your governance structures will be examined; it is whether they will hold up when they are. This post outlines the specific accountability gaps regulators are watching, and the practical actions decision-makers, CEOs, CTOs, COOs, and board directors must take to protect their licence to operate and sustain investor confidence.

Why This Is Urgent for Every FinTech Company Right Now

The fintech industry has matured past the “move fast” era. Whether you are scaling a fintech app, running a regional player like Apex Fintech Solutions, or competing at events like the Singapore FinTech Festival, regulators now expect governance structures equivalent to traditional financial institutions without the legacy infrastructure to excuse gaps.

Three converging pressures are driving this urgency:

- Regulatory convergence : bodies in the UK (including fintech Scotland ecosystems), EU, US, and Singapore are aligning on operational resilience, AI oversight, and accountability frameworks.

- Investor scrutiny : boards without documented governance structures struggle to close funding rounds as institutional investors conduct deeper ESG and compliance due diligence.

- Intelligent business transformation : as organisations automate decisions using AI and data platforms, accountability for those automated decisions must live somewhere at board level.

What Is the Governance Gap and What Does It Actually Mean for FinTech?

FinTech meaning in regulatory terms has shifted. It is no longer simply financial services delivered through technology. Regulators now define financial technology companies by the risk they carry, not the products they build. The governance gap is the distance between:

- The decisions your technology makes or enables

- The human accountability structures that own those decisions

This gap typically appears in three areas:

- AI and algorithmic accountability, who at board level owns the outcomes of automated credit, fraud, or compliance decisions?

- Third-party and supply chain risk, are your board-level risk committees examining fintech partners and vendors with the same rigour applied internally?

- Data governance, does your board have a named DPO or Chief Data Officer with direct reporting lines, documented mandates, and escalation paths?

How to Identify Whether Your Board Has a Governance Gap

Ask these questions in your next board session:

- Can your board name without hesitation who is accountable for each AI-driven decision your platform makes?

- Does your risk committee review third-party fintechs and technology vendors against the same standards applied to internal teams?

- Is there a documented escalation path from operational technology decisions to board-level accountability?

- Have you mapped your governance structure against the current regulatory expectations in every jurisdiction you operate in?

- Does your board receive regular, structured updates on fintech news and regulatory developments, not just quarterly summaries?

If the answer to any of these is “no” or “I’m not sure,” the gap is present.

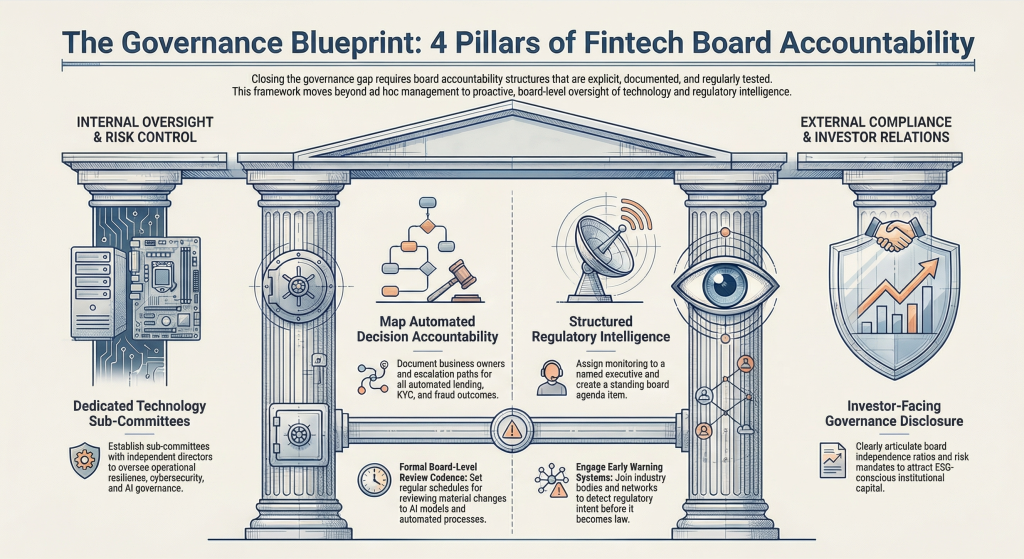

The Accountability Structures That Actually Protect Your Licence

Closing the governance gap requires building accountability structures that are explicit, documented, and regularly tested. Here is what boards operating in high-scrutiny environments are implementing:

1. Board-Level Technology and Risk Sub-Committees

Do not leave technology governance to management alone. High-performing fintech boards are creating dedicated sub-committees, populated by independent directors with financial technology experience, that own:

- Operational resilience standards

- Cybersecurity posture and incident response authority

- AI model governance and outcomes monitoring

2. Clear Accountability Mapping for Automated Decisions

For every automated decision your platform makes lending, KYC, fraud detection, pricing ,document:

- The business owner accountable for model outcomes

- The escalation path when outcomes fall outside expected parameters

- The board-level review cadence for material model changes

This is not optional for fintech companies pursuing institutional partnerships or preparing for regulatory examination.

3. Structured Regulatory Intelligence Processes

Boards that rely on ad hoc awareness of regulatory change are perpetually behind. Build a structured process:

- Assign ownership of regulatory monitoring to a named executive

- Create a standing board agenda item for regulatory horizon scanning

- Engage in industry bodies, fintech meetup networks, associations, and working groups are early warning systems for regulatory intent

4. Investor-Facing Governance Disclosure

As fintech futures are increasingly shaped by ESG-conscious institutional capital, boards need to be able to articulate governance structures clearly in investor communications. Document your:

- Board composition and independence ratios

- Risk committee mandates and meeting frequency

- Governance improvement roadmap tied to business milestones

The Role of Intelligent Business Transformation in Closing the Gap

Governance gaps often widen during transformation. When fintech companies implement new platforms, automate workflows, or enter new markets, accountability structures must evolve in parallel, not catch up after the fact.

Intelligent business transformation means building governance into the architecture of change, not bolting it on at the end. This includes:

- Embedding compliance checkpoints into technology deployment pipelines

- Ensuring every new fintech app or platform capability has a named governance owner before launch

- Aligning transformation roadmaps with regulatory examination cycles in your key markets

What Regulators Are Actually Looking For

Across regulatory examinations globally, the pattern is consistent. Examiners are not looking for perfection, they are looking for evidence of:

- Intentional governance design : you built your accountability structures deliberately, not reactively

- Board-level engagement : directors can speak to governance decisions, not just management

- Continuous improvement : you identify gaps and act on them before they become findings

Fintech careers increasingly require governance literacy at every level. Boards that build this culture attract stronger talent, close funding rounds with greater confidence, and enter regulatory examinations from a position of strength.

Action Plan: What Boards Need to Do in the Next 90 Days

- Week 1–2: Commission a governance gap assessment mapped against current regulatory requirements in your operating jurisdictions

- Week 3–4: Review board sub-committee structures and assign explicit technology and AI accountability

- Month 2: Document accountability mapping for all automated decision systems

- Month 3: Build regulatory horizon-scanning into board reporting cadence and investor communications framework

Frequently Asked Questions

Q. What is a fintech company’s board governance obligation under current regulation?

A. FinTech companies are expected to maintain governance structures equivalent to regulated financial institutions, with explicit board-level accountability for technology risk, automated decisions, and operational resilience — regardless of company size.

Q. What does fintech mean in a regulatory context today?

A. Regulators define fintech by the risk profile of the services delivered, not the technology used. Any company using automated systems to make or influence financial decisions carries governance obligations tied to those decisions.

Q. How do fintech boards protect investor confidence during regulatory scrutiny?

A. By maintaining documented, board-level accountability structures that can be clearly articulated to both regulators and institutional investors, including AI governance, third-party risk oversight, and structured regulatory intelligence processes.

Q. What is the first step to closing the governance gap in a fintech company?

A. A structured gap assessment that maps your current accountability structures against regulatory expectations in every jurisdiction you operate in. This should be board-commissioned and independently reviewed.

200OK Solutions delivers intelligent business transformation for FinTech organisations navigating regulatory complexity. Learn how we help boards build governance structures that protect licences and accelerate growth at 200oksolutions.com.

You may also like: Embedded Finance: The New FinTech Partnership Economics